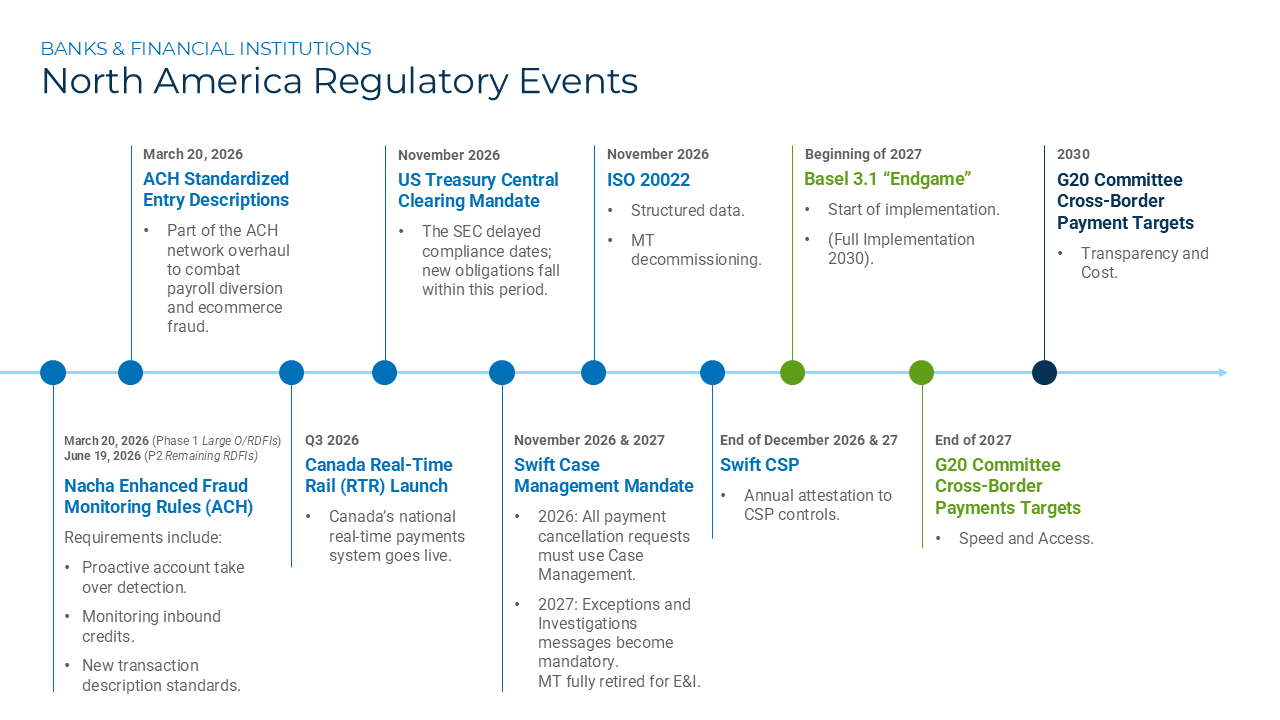

North America is entering a pivotal moment in payments. Across the United States and Canada, financial institutions are navigating changing regulations, rising fraud pressure, and growing expectations for real-time, transparent payments.

Yet while the U.K. and Europe are tightening protection frameworks, mandating payments verification and instant payments readiness, the North American market is moving more slowly, and in some cases even a bit backwards. Or so it can seem.

The impact of this “regulation gap” reaches far beyond compliance. It affects customer trust, competitive positioning, and whether institutions can realistically deliver on the G20 cross-border payment roadmap for speed, cost, transparency, and inclusion.

And as Bottomline’s latest research shows, institutions that take proactive steps today, even without regulatory mandates, are emerging stronger for it.

The U.S. -- Deregulation Meets Rising Expectations

Finextra’s report US Regulation Pulse Check 2026 reveals a contradiction at the heart of U.S. regulatory sentiment. On paper, deregulation brings flexibility: 51% of institutions expect a positive impact from the current deregulatory agenda. Yet only 8% believe this new environment is free of downsides. When asked about the risks, institutions point to the very foundations of market instability: illicit finance, reduced oversight, systemic risk, and, critically, erosion of consumer protection.

This tension is compounded by the potential shutdown of the Consumer Financial Protection Bureau (CFPB), which could derail open banking under Section 1033 and leave consumer rights to market discretion rather than with regulatory guardrails. The result? A landscape where financial institutions must shoulder more responsibility for consumer trust at the very moment that regulation is retreating.

But the story isn’t one of institutions ignoring risk. Finextra’s report shows that nearly 95% of responding FIs expect to spend at least 5% of EBITDA on compliance, and 88% are upgrading AI or automation for fraud and compliance monitoring, reflecting an industry that sees technology as the best way to mitigate uncertainty.

What’s missing from this mix is national direction around fraud prevention and customer protection. So, in a deregulated environment, banks that voluntarily set higher standards will become the new reference point for trust, almost by default.

It’s worth noting, however, that the US regulatory position it starting to evolve. The GENIUS Act introduces clearer federal guardrails for payments via stablecoins in the US, offering a more structured framework than has ever previously existed.

Canada -- Methodical, But Falling Behind the Curve

Canada’s regulatory progress is steady, but slow. Whether it is consumer-directed finance or the long-anticipated Real Time Rail, cautious rollouts have kept risk low but have also limited innovation and delayed benefits to all stakeholders.

Meanwhile, the pain points identified by global banking leaders in Bottomline’s Competitive Banking Report, especially around cross-border payments, are becoming hard to ignore for Canada. Slow or uncertain payment arrival times and limited visibility remain among the biggest challenges for senders and receivers. These are issues that richer data, stronger verification tools, and real-time interoperability can solve.

Canada’s best opportunity lies in leapfrogging. By adopting modern frameworks such as Verification of Payee (VoP), digital identity signals, and ISO 20022-driven transparency ahead of regulation, Canadian banks can differentiate themselves and remove friction that global corporates increasingly won’t tolerate.

What G20 Targets Reveal About the Regulation Gap

The G20’s roadmap for cross-border payments (faster, cheaper, more transparent, more inclusive) has never been about infrastructure alone. It depends heavily on the underlying confidence participants have in the payments journey. And this is where regulatory differences can impact performance.

In the U.K., for example, mandatory reimbursement for authorised push payment fraud and schemes like Confirmation of Payee (CoP) have materially reduced fraud and boosted consumer confidence. Broad CoP adoption now covers 400 financial institutions, about 99% of U.K. Faster Payments volume, and has contributed to a meaningful drop in APP fraud losses.

Europe is also following suit with Verification of Payee (VoP) being integral to the European Payment Council’s SEPA Inst Mandate, which saw almost 3,000 PSPs go live as part of phase one in October 2025. Remaining non-euro countries are due to comply by October 2027. APAC is also accelerating this effort, with national rollouts for pre-validation already underway in Australia, and expected in New Zealand

In North America, these protections don’t exist at scale. U.S. Reg E still doesn’t cover authorised push scams (the fastest growing fraud type globally), and neither the U.S. nor Canada has mandatory reimbursement rules or universal payee verification standards. FIs are left to set their own policies, creating vastly different experiences for customers who now expect reliability, consistency, and transparency.

Hopefully, this makes a compelling argument for the industry to start approaching Bank Account Verification (BAV) more seriously.

This gap directly affects the G20’s four key outcomes:

- Speed: Consumers hesitate to use faster payments when protections are weak.

- Cost: Poor data quality and high error rates increase operational overhead.

- Transparency: Lack of tracking and verification increases disputes and delays.

- Inclusion: Unprotected customers, especially the unbanked, bear disproportionate risk.

The result of this lack of confidence is that fewer payments professionals will use services that the G20 framework aims to unlock.

Insights from Bottomline’s Global Report: Protection Creates Advantage

As the U.S. and Canada debate regulatory direction, global institutions are already showing what ‘good' looks like. In Bottomline’s Competitive Advantage in Banking and Payments report, top performers, called “Payment Pioneers”, share three characteristics:

- They treat ISO 20022 as a strategic asset, not a compliance project. Nearly 70% already have multiple use cases in production, using richer data for better automation, reconciliation, sanctions screening and fraud detection.

- They implement payee verification ahead of deadlines, recognising that reducing misdirected payments and APP fraud improves satisfaction, reduces call centre volumes, and drives adoption of instant rails. Some already have CoP/VoP solutions in place, even where regulation hasn’t mandated them.

- They modernise through SaaS, replacing fragile legacy infrastructure with modular, cloud-based systems that support resilience, real-time data, and vendor consolidation/simplification. Institutions cite operational efficiency and continuity as top reasons for transitioning to SaaS.

These aren’t compliance moves, they’re commercial strategies.

Fraud mitigation remains a top priority on product roadmaps worldwide because fraud directly impacts customer satisfaction. Multiple global surveys show that customers who suffer losses due to payment fraud often leave their FI permanently.

Conversely, banks that take on more of the fraud burden tend to see improved retention, lower dispute-handling costs, and stronger acquisition performance. In simple terms, protection builds trust, and trust builds value.

Why North American Financial Institutions Shouldn’t Wait for a Mandate

In the U.K. and E.U., regulators drive the payments agenda. In North America, the market does. This creates an opportunity for North American banks to lead by delivering the experiences business customers already expect:

- Payment journeys that verify the recipient in real time.

- Fraud processes that favour the customer, not the institution.

- Data-rich messaging that reduces failures and lowers friction.

- Cross-border payments with predictable timelines and transparent tracking.

Institutions that deliver these outcomes, ahead of deadline, will be the ones corporates choose and consumer's trust.

Bottomline’s global data shows an industry moving from reactive compliance to proactive experience design, using fraud protection, data standards, and real-time payments as the foundation for competitive differentiation.

That shift is precisely what North America needs.

Trust Is the New Battleground

The debate over whether the U.S. and Canada are “suffering” from lighter regulation misses the point. Regulation is no longer the main driver of consumer protection, transparency, or trust. Institutions are.

Those that embrace payee verification, structured data, digital identity, real-time fraud controls, and resilient SaaS infrastructure will shape the direction of the market, not merely comply with it. And in doing so, they’ll capture the benefits that stronger protections bring: lower attrition, satisfied customers, reduced fraud, and a competitive edge in the fast-moving global business payments sector.

In the race toward G20-level payments, trust is the fuel. Customers reward the institutions that prioritise it.

Share