Fraud and credit monitoring to incorporate risk-based processes and procedures.

Get Nacha-Ready for 2026. No Extra Headcount Required.

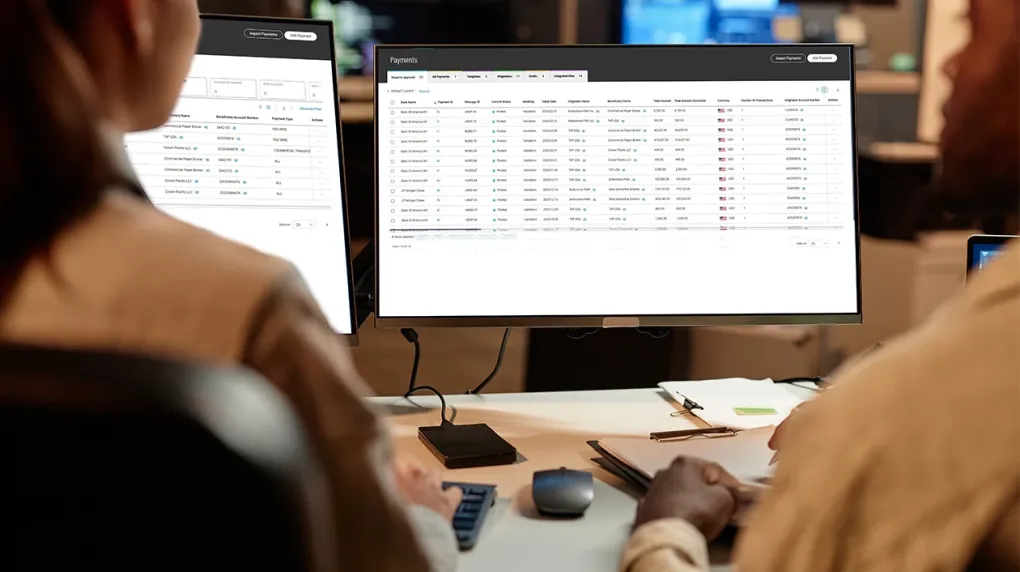

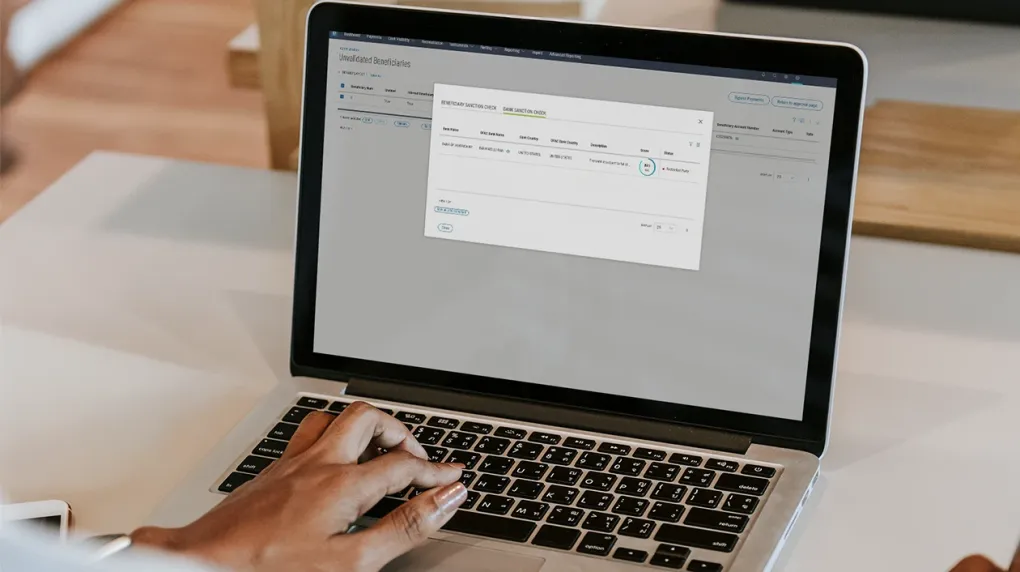

Bottomline’s Payments Hub helps treasury and payments teams standardize workflows, enforce security policies, and build audit‑ready controls - so you can keep moving money as fast as Nacha’s risk management rules expand in 2026.

Become Nacha-Ready in Weeks

Implement 2026 Operating Rules, Fight Fraud, and Master Payments

Many treasury and payments teams are already juggling disconnected systems and bank portals – so there are bound to be gaps in governance, compliance, and visibility. Now add Nacha’s 2026 risk management updates – which require specific features be available in technology, operations, and risk management. Non-compliance can mean fines, reputational damage, and regulatory scrutiny. Bottomline’s Payments Hub gets you Nacha-ready without a heavy lift. Robust fraud monitoring controls are built right into your workflow, making compliance a by-product of how ACH payments run.

What’s Changing in 2026 with Nacha

Nacha’s 2026 rules updates are aimed to prevent, detect, and respond to ACH fraud. Here are the changes treasury and payments professionals need to be aware of:

Standardized mandatory descriptors of “PAYROLL” and “PURCHASE” for certain ACH transactions.

Required International ACH Transactions (IAT) classification for any transaction flowing outside the U.S.

9:00 a.m. funds availability for all non-Same Day ACH credits.

Move Money with Confidence.

Not Crossed Fingers.

Payments Hub centralizes every payment - domestic, international, bank-to-bank, intracompany - in one place. It integrates with your ERPs, banks, and global bureaus.

So payments move through a single system instead of scattered portals, spreadsheets, and workarounds.

As payments flow, Payments Hub works in the background enforcing the controls Nacha expects - without slowing you down:

- Embedding risk-based fraud monitoring into ACH workflows

- Enforcing approval, security, and signer controls automatically

- Maintaining audit-ready proof without manual effort

Get Nacha-Compliant Payments Up and Running in as Few as 12 Weeks

Stay Compliant at Every Step

1. Before Payments

2. As Transactions Get Processed

3. As Compliance Rules Evolve

Join the Companies Mastering Compliance with Payments Hub

Nacha and Payments Hub FAQs

What is Nacha?

Nacha is the governing organization that oversees the Automated Clearing House (ACH) Network which is the centralized U.S. financial network used for electronic funds transfers between banks and credit unions. The non-profit formally known as the National Automated Clearing House Association sets rules and standards for safe and efficient electronic payments in the United States.

What are the 2026 Operating Rules?

Nacha Operating Rules define the roles and responsibilities of U.S. financial institutions participating in the ACH Network. In March of 2026, ACH participants will be expected to start implementing risk-based fraud monitoring, expand ACH credit-monitoring responsibilities, and adopt new controls such as standardized entry descriptions and updated return codes.

What are examples of ACH fraud?

ACH fraud can include a variety of attempts such as altered invoices, fake payment requests, unauthorized debits using bank account and routing numbers, data breaches that can allow fraudulent transfers, and check kiting where criminals move money between accounts. Fraudulent initiatives are consistently changing.

How long does it take to become “Nacha-ready"?

Implementations that are “Nacha-ready” vary depending on the number of bank and ERP integrations required. We have helped clients get their Payments Hub up and running in as few as 12 weeks.

What are “risk-based” fraud monitoring controls?

"Risk-based" fraud monitoring controls are tailored measures designed to identify, detect, and mitigate fraud by focusing resources on the highest-risk transactions and behaviors. Instead of treating all activities equally, this approach uses assessments to apply stricter, often automated, scrutiny to suspicious, large-dollar, or unusual transactions while reducing checks on low-risk activity.

Who uses Payments Hubs?

Payments hubs are primarily used by financial institutions (banks, credit unions, financial technology companies) and large, multinational corporations to centralize, automate, and manage complex, high-volume payment transactions across multiple channels and rails. They act as “mission control” to streamline operations, reduce costs, and ensure regulatory compliance.

What are International ACH Transactions (IAT)s?

IATs are electronic, cross-border payments sent to or received from a financial agency outside the United States via the ACH Network. Mandated by Nacha and the Office of Foreign Assets Control (OFAC), these transactions provide increased transparency for anti-money laundering compliance by including detailed, mandatory information about the originator and receiver.

Ready to centralize payments and take compliance off your plate?

Complete the form and we’ll be in touch ASAP.

Thank You!

We'll be in touch